New Homes & Renovation

After waiting two or three years for a pre-sale unit, handover day is finally here — and the feeling is complicated: excitement mixed with worry that something will go wrong right at the finish line. How long does handover actually take? How does the final payment work? What even is "mortgage verification"? Without a clear handle on these, it's easy to get pushed around by the timeline.

This article lays out the full handover timeline, the final payment and retention payment, the documents needed for mortgage verification, and how the handover date gets set. All ratios and day counts here follow the contract terms and the lending bank's requirements — they won't apply identically to every case.

Key takeaway: Handover isn't a single-day event — it's a process running from mortgage verification through inspection to final handover. Under Taiwan's Ministry of the Interior's standard pre-sale contract, buyers have the right to withhold 5% of the total property price as a "handover retention payment," released only after repairs are completed and both parties re-inspect and approve them (Ministry of the Interior regulations, 2026) — the single most important protection for buyers.

Here's an anchor point to start with: under Article 15 of the standard pre-sale contract, the seller must notify the buyer to proceed with handover within six months of obtaining the occupancy permit (Ministry of the Interior regulations, 2026). In practice, pre-sale units typically take about six months from mortgage verification to handover, while resale units are much quicker — roughly one to two weeks (Dajia Realty, 2026).

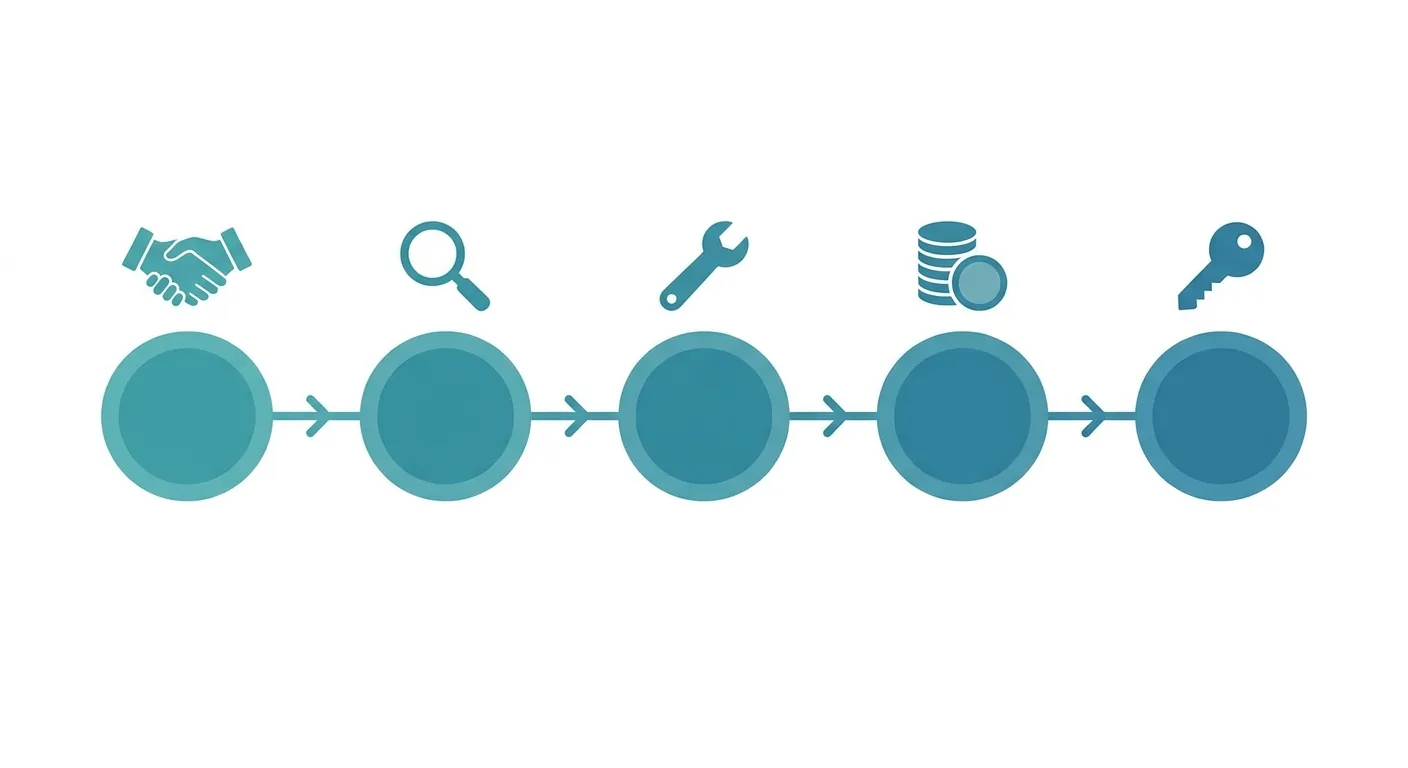

The handover process generally follows this order:

Caption: Five steps of handover — ① bank mortgage verification ② inspection and defect list ③ repairs and re-inspection ④ final payment disbursed ⑤ handover and keys

So what actually determines "how long"? Mainly the number of defects found during inspection and how many rounds of re-inspection it takes. Few defects that clear on the first pass means a short timeline; lots of defects requiring several rounds of re-inspection naturally stretches it out.

One thing worth stressing: the home inspection is the single most critical checkpoint before handover. Every defect needs to be documented in writing on the defect list, and you shouldn't sign off until repairs are done and re-inspection passes — don't rush to accept it. Actual timing depends on the developer and the specific case, so don't stress if you hear someone else got their keys in "two weeks" — your case has its own pace.

This handover window is best planned alongside your renovation timeline. To get a sense of how long post-handover renovation takes, see New Build Renovation Sequence and Timeline; for the full sequence from customization to move-in, see The Complete Overview From Pre-Sale Customization to Handover.

Let's untangle two terms people often mix up. Under Article 13 of the standard pre-sale contract, buyers have the right to withhold 5% of the total property price from their own funds as a "handover retention payment," paid only after repairs are completed and both parties re-inspect and approve them (Ministry of the Interior regulations, 2026). That 5% is a figure set explicitly in regulation to protect buyers.

As for the "handover installment" within a pre-sale unit's payment schedule, the ratio and amount vary by contract and don't generalize across projects — read every clause carefully when you sign.

Caption: Common pre-sale installments — deposit, contract deposit, groundbreaking payment, construction-period payments, handover payment; each stage's ratio follows the contract, and the retention payment is 5% of the total property price

How does the final payment tie into loan disbursement? Most people use their mortgage disbursement to cover the final payment, so the timing of verification, appraisal, and disbursement needs to line up with the handover date — otherwise payment gets stuck.

There's a key sequencing point here. The retention payment is typically released only after defect repairs are completed and re-inspection passes. If the defects haven't been fixed yet, don't rush to release the final payment — that 5% is your leverage for negotiating repairs, and letting it go too early means losing it.

Ever wondered: if the inspection doesn't pass, can you withhold the final payment? Yes — you can insist on withholding it; that's exactly what the retention payment mechanism is designed for. To plan your pre-handover renovation budget alongside this, pair it with the post-handover renovation budget template; if you're still in the customization phase and want to fold customization surcharges into your cost estimate, see How Pre-Sale Customization Costs Are Calculated.

Here's the plain-language version: mortgage verification is the step where the bank and the borrower confirm the loan contract, usually completed before handover, and it's a required step before disbursement. The typical standard process runs: verification → initial inspection → re-inspection → title transfer → disbursement → handover complete (PULO Renovation Platform, 2026). Without verification, the bank won't release the funds.

Caption: Commonly needed for mortgage verification — ID documents, personal seal, proof of financial standing; the actual list follows your lending bank's requirements

The documents commonly needed for mortgage verification fall into a few categories: ID documents, personal seal, proof of financial standing, and similar items. That said, the specific list follows what your lending bank requires and varies from bank to bank — the safest move is to call your loan officer ahead of time and ask.

There's a timing trap that's easy to fall into here. Verification, appraisal, and setting up the mortgage lien all happen in sequence and each takes processing time. Start too late, and you may well hit your handover date with the loan still not disbursed.

My suggestion: confirm the whole schedule early with your title agent and bank. Ask upfront what comes first, what comes after, and how many days each step takes, so you're not scrambling on handover day. This part is procedural — the advice here is simply to follow the standard steps, without recommending any particular bank's program.

Where does the handover date actually come from? Under the standard contract, the seller must notify the buyer of handover within six months of obtaining the occupancy permit (Ministry of the Interior regulations, 2026). In other words, the handover date is mostly set by the developer once construction is complete and the occupancy permit is obtained — buyers can coordinate with the developer within a reasonable range, but are constrained by construction progress and don't have full say over the date.

As for "is it okay to have handover during Ghost Month, should you pick an auspicious date" — that's a matter of tradition, not a legal requirement. Some people care a lot about it, others follow the process without a second thought; respect your own beliefs and decide for yourself.

In practice, plenty of people take a middle path: follow the bank and developer's process for the actual handover, then separately pick a date for a formal house-warming. That way, you don't hold up the disbursement timeline while still honoring the tradition that matters to you. For how to plan a house-warming date and furniture checklist, continue on to Choosing an Auspicious House-Warming Date and Furniture Checklist After Handover.

One last easy-to-miss reminder: the handover date, final payment disbursement, moving day, and house-warming all need to be scheduled together — don't let the timelines collide. We've seen people lock in a handover date only to find the moving company fully booked and the loan not yet disbursed — total chaos. Laying out this timeline early smooths things out considerably. Once handover is done and you start planning renovations, you can use Roomfit to import the developer's floor plan and place furniture at true 1:1 scale, working backward to outlets and traffic flow, catching sizing issues before construction even starts.

Keep three principles in mind and handover stays under control. First: the inspection is everything — don't rush to release that 5% retention payment until defects are fixed and re-inspection passes. Second: the final payment mostly relies on mortgage disbursement, so verification, appraisal, and disbursement need to line up with the handover date. Third: schedule handover, moving, and house-warming together — don't let each run on its own track.

My own takeaway: handover isn't scary if it's slow — it's scary if it's chaotic. Breaking the process into clear, understandable checkpoints and working through them one at a time is more reassuring than anything else. If you're renovating after handover, place your furniture in Roomfit first and catch sizing and outlet issues before construction starts, so you don't end up redoing work later.

Under Article 13 of Taiwan's standard pre-sale contract, buyers have the right to withhold 5% of the total property price as a "handover retention payment," paid only after repairs are completed and both parties re-inspect and approve them (Ministry of the Interior regulations, 2026). That 5% is a figure set explicitly in regulation to protect buyers. As for the "handover installment" within the payment schedule, its ratio and amount follow the contract — read every clause carefully when signing.

Under the standard contract, the seller must notify the buyer of handover within six months of obtaining the occupancy permit (Ministry of the Interior regulations, 2026). In practice, pre-sale units typically take about six months from verification to handover, while resale units are much quicker — roughly one to two weeks (Dajia Realty, 2026). The actual timing depends on the number of defects found and how many rounds of re-inspection are needed — few defects means it moves fast, several rounds of re-inspection means it's slower, and it depends on the developer and the specific case.

Yes, you can insist on withholding it. The handover retention payment (5% of the total property price) is specifically designed to let buyers hold that money until defects are repaired and re-inspection passes (Ministry of the Interior regulations, 2026). So the inspection must produce a written defect list — repairs and passing re-inspection come before the final payment is disbursed. Don't release the payment before defects are fixed; that 5% is your leverage for negotiating repairs.

Commonly needed documents include ID documents, personal seal, and proof of financial standing, though the specific list follows your lending bank's requirements and varies by bank. Verification, appraisal, setting up the mortgage lien, and disbursement happen in sequence and each take processing time; the typical standard process runs verification → initial inspection → re-inspection → title transfer → disbursement → handover (PULO Renovation Platform, 2026). It's best to confirm the schedule early with your title agent and bank, to avoid hitting your handover date with the loan still not disbursed.

This is a matter of tradition, not a legal requirement — some people care a lot, others follow the process without a second thought; respect your own beliefs and decide for yourself. The handover date is mostly set by the developer once construction is complete and the occupancy permit is obtained (under the standard contract, notice must be given within six months of obtaining the occupancy permit, Ministry of the Interior regulations, 2026), leaving buyers limited room to negotiate. In practice, plenty of people follow the standard handover process and separately pick a date for a formal house-warming, balancing the disbursement timeline with the traditions that matter to them.

Arrange furniture in your space at true 1:1 scale with Roomfit and see exactly how much walkway is left — no install, no sign-up.

Start with Roomfit →